DAY-TO-DAY DEVELOPMENTS in the world economy have become increasingly complex and global in their implications. From Greece to China to Russia, economic shocks are now of greater concern because around the world, traditional policy tools have already been used and financial resources depleted to help economies recover from the last downturn. As a result, strategic decisions have become more consequential.

Shocks are inevitable, but strategists must find ways to extract the signals from the noise to understand what lies over the horizon.Three interlinked factors have the potential to shift the global economy from one long-term outcome to another. First, in the near term, the major economies continue to struggle to achieve self-sustaining growth in aggregate demand. This continues despite years of monetary and fiscal stimulus, as well as the recent drop in oil prices.

Second, the world’s major economies face long-term structural challenges, including rising debt loads, aging populations, and inadequate or aging infrastructure. Success or failure in resolving these challenges will determine the speed of long-term growth in these economies. Third, the world’s major economies have diverged in the last few years. In the past, global integration has driven convergence, but the prospects for further integration have become less certain. The global financial shock was followed by years of weak growth and concerns over rising inequality, and the path to renewed and stronger growth remains elusive. Given the consequences of these interlinked factors, it is small wonder that near-term developments have taken on oversized importance.

We believe that three sets of forces will shape the global economy over the coming decade. The first two are stimulus policies and shifting energy markets. These are near-term forces, whose effects are felt on a daily basis. The next two forces, urbanization and aging, are powerful, inexorable trends aggravating ongoing structural challenges. Finally, there are two forces of uncertain and variable magnitude: technological innovation and global connectivity. All of these trends could intermittently disrupt and transform sectors. We will examine each in turn.

1. The Near-Term Factors

Stimulating aggregate demand. Of immediate concern is the persistent problem of weak aggregate demand relative to overall economic capacity. The International Monetary Fund estimates that production in the ten largest advanced economies was two per cent below potential in 2014. This gap was smaller than it had been in 2009 (3.3 per cent) but significantly worse than the surplus of 0.8 per cent that prevailed in the early 2000s. All major economies except China experienced significantly weaker demand in the aftermath of the global financial crisis. Many governments and central banks responded with fiscal and monetary stimulus programs that fostered the low real-interestrate environments which have endured for over five years. The McKinsey Global Institute reviewed the recent performance of advanced economies and found that they had all increased rather than reduced their overall debt levels — in some cases, by more than 50 per cent.

Complicating the picture is the question of whether real interest rates will remain low. Persistently-low interest rates encourage investors to search for yield and safety, creating the preconditions for asset bubbles and further volatility in international financial flows. Economists are concerned that unconventional monetary policies have distorted rather than bolstered the demand picture. In the United States, for example, the Federal Reserve signaled for months that it would raise rates by the end of 2015, heralding a return to a more conventional, interest rate–driven monetary policy. In the interim, however, results were tepid, and a rate hike has been further delayed. The challenges faced by the Federal Reserve in timing rate increases will be encountered in the eurozone and Japan in due time. Furthermore, demand in major markets remains weak enough that a misstep in any one of them will be felt by the others.

Energy-market transformations. Oil prices fell by 50 per cent in the latter half of 2014. Even after a slight rebound, they remained well below average levels of the past five years. For energy consumers, lower energy prices have provided a welcome respite; but for producers, they challenge fiscal stability. The break-even oil price — the price at which a fiscal surplus turns into a deficit — is estimated at $57 for Kuwait and $119 for Algeria. Countries have so far managed the crunch by drawing down reserves and through exchange-rate movements, but these are short-term actions and direct fiscal adjustment lies on the horizon. Elsewhere, the fall in oil prices is slowing further investment in energy sectors, notably unconventional oil and gas.

Global energy intensity has fallen over the past several decades, so oil-price shocks are felt differently in different parts of the world. The energy productivity of the ten largest advanced economies today is 74 per cent of what it was in 1980. Beyond the advanced economies, however, the picture changes. Thanks to the increasing size of the emerging economies, world energy productivity was able to rise by 33 per cent between 1980 and 2002 (remaining relatively flat thereafter).

In assessing the ultimate impact of recent energy-market shifts, strategists are seeking to discover what will happen not in the next year, but in the next decade. Only on two other occasions during the past 30 years, in 1985 and 2008, did the oil price fall as steeply as it did in 2014. The recoveries from these two events were very different affairs and are instructive for today. In 1985, excess production capacity led to stable prices for nearly a decade after the initial price decline. The 2008 decline in prices was part of the global financial crisis; prices dropped precipitously and then quickly rebounded as demand recovered, especially in emerging markets.

Persistent demand weakness and falling oil prices are the stuff of daily headlines, but associated effects could drive alternative economic outcomes for the next decade. The complication is that deeper forces are at work.

The fall in oil prices is slowing further investment in energy sectors, notably, unconventional oil and gas.

2. The Inexorable Factors

Unlike the impact of demand stimuli and energy-market shifts, the effects of urbanization and aging are predictable and are tilting the global economy in one general direction: towards emerging markets.

Rapid urbanization. From Brazil to China, emerging economies are urbanizing with unprecedented rapidity. Rural populations are responding to rising industrial opportunities and burgeoning growth, and the economic weight of cities in the world economy continues to rise. McKinsey research indicates that 46 of the world’s 200 largest cities will be in China by 2025, a sign too of the eastward migration of the global economy’s centre of gravity.

In recognition of its urbanization challenge, the Chinese government is moving with astonishing speed to meet its climate goals, because the pollution produced by outmoded power generation and manufacturing is starting to interfere with the quality of life in urban areas. India is facing similar and intensifying urban challenges, but has not yet moved with China’s determination.

Demographic pressures. The labour force on which economic activity depends is both aging and shrinking. It is expected to contract by 11 per cent in China by 2050, even as the country’s economy expands. The shrinkage in continental Europe is expected to be even more dramatic. Furthermore, as life spans are growing and birthrates falling, an aging working population in advanced and emerging economies will be supporting ever higher numbers of retirees. Among the major economies, only the U.S. has a demographic profile favourable to long-term economic growth. For the rest of the leading economies, expected productivity improvements will not bridge the gap. Without a fundamental economic and cultural shift that favours continued participation of older workers and the introduction of more women workers and immigrant labour, many economies would face serious growth constraints within ten years.

3. The Uncertain Factors

The potential impact of the final factors in our review are less certain than the effects of urbanization and aging.

Technological innovation. Technological innovation has reached a level in the major economies where significant structural changes are in process or have already occurred. Digitization has transformed the telecommunications, media, financial services and retail sectors. High-tech innovations in robotics and 3-D printing could enable mature and emerging economies alike to boost labour productivity and rapidly expand industrial horizons, while also shifting global trade patterns.

Global connectivity. Trading relationships are increasingly dense and complex, and they have rebounded rapidly since the global downturn. Today, China is a peerless world-trade hub and Latin American, Indian and Middle Eastern trade has risen in world-economic weight. Among other factors, the recapitalization of banks, regulatory change, and monetary stimulus have exercised countervailing effects on financial flows, which remain well below pre-crisis levels. Concerns about the transmission and impact of financial shocks remain high on the global regulatory agenda.

More than 20 years have passed since the conclusion of the last round of multilateral trade negotiations in 1994. More economies have been opened since then, and the scope of trade agreements has widened. The focus in developed economies has shifted toward the opening of investment opportunities and easing of restrictions on services; in emerging markets, agricultural subsidies have been a priority. These areas have proven especially intractable in a multilateral context, but regional and bilateral trade agreements of widening scope have nonetheless proliferated since 1994.

As the last two decades have demonstrated, increasing international trade flows can reshape national growth trajectories. However, a rising caution pervades public debate about deepening economic linkages among countries. The principal concerns go beyond the potential impact on growth, even within specific sectors. The reservations are more focused on the wider question of whether nations can agree on global rules that are appropriate and supportive for an evolving economy.

Four Possible Scenarios

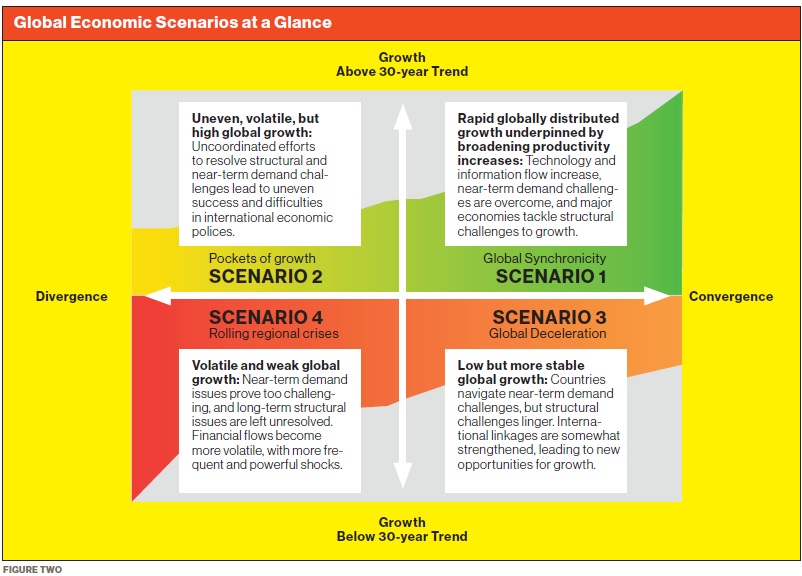

Our scenarios for the coming decade are shaped by the three tightly linked sets of factors outlined above, and the interaction of these factors will govern a number of crucial outcomes. Is weak growth in advanced economies going to undermine the will to open more politically sensitive markets and sectors? To what extent will inadequate infrastructure or restrictive markets stall growth in emerging countries? How will falling commodity prices complicate efforts to diversify commodity-driven economies?

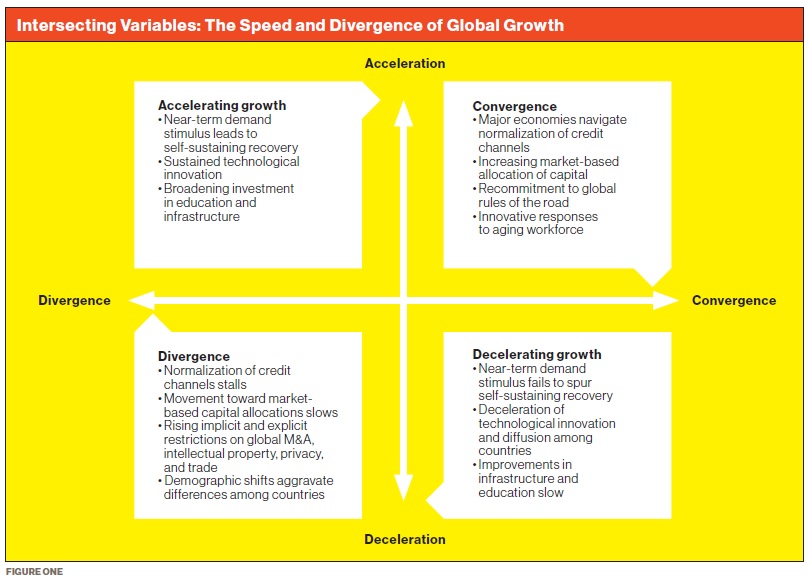

The longer-term factors discussed above — urbanization, aging, technological innovation, and global connectivity — anchor our four scenarios, while the near-term factors — monetary stimulus and energy prices — inform the path to the longer-term outcomes. These dynamics have been framed by the intersection of two axes (see Figure One). The vertical axis measures the acceleration or deceleration of growth and thus how well (or poorly) economies have tackled their long-term structural challenges. Successful economies drive up productivity and overall growth. The horizontal axis measures the extent to which global growth is convergent. This is determined by a combination of near- and longer-term factors.

Countries can converge toward higher (or lower) growth rates, for example, according to how successful they have been in implementing and then unwinding their monetary and fiscal stimulus. In the long term, increasing convergence is also determined by the global evolution of economic rules of the road, covering the extent of economic activity, including goods and services, migration, investment, and intellectual property rights.

A convergent world would not be impervious to shocks, but it would be better able to absorb them. Higher global systemic resilience means that individual economies can recover more quickly. Divergent outcomes, on the other hand, result when the policies of individual countries are at odds, creating internal systemic imbalances that can magnify the effects of a shock in a particular country. Divergence can also slow the movement of shocks across borders — a movement that, unfortunately, is common in an interconnected world.

A final consideration is the historical pace of global growth, which provides context for the scenarios. This indicator has been remarkably stable since the mid-1980s. The rolling ten-year average real growth rates hovered between 3.4 and 2.7 per cent.

SCENARIO 1

GLOBAL SYNCHRONICITY: CONVERGENCE AND RAPID GROWTH

In this scenario, the global economy experiences the most robust long-term growth it has seen in more than three decades, reaching 3.7 per cent per year through 2025. The U.S., the eurozone, and Japan are able to make the transition to more sustainable growth while exiting from their monetary stimuli with minimal disruption. Likewise, policy makers in China implement incremental changes and guide economic growth smoothly and gradually downward to a sustainable level. India emerges as the fastest-growing economy over this period as it rides a wave of reform, investment, and robust demographics. By 2025, the global economy will have grown to $90 trillion in constant 2015 dollars, from $62 trillion in 2015.

As global growth gathers momentum, liquidity from unconventional monetary policies is gradually absorbed or withdrawn in the U.S., the eurozone, and Japan. Proliferating trade agreements lead to the lowering of barriers in critical service industries and to revivals of cross-border activity and technology transfer. The rapid diffusion of innovation, bolstered by broader global trade arrangements, boosts the share of exports in GDP for the G-20 from 25 per cent today to 29 per cent by 2025, or roughly at the growth rate of the early 2000s.

Financial-sector reforms in emerging economies foster more market-driven and robust capital markets. Global interest rates return to the ‘old normal’ levels of the pre-crisis years. Energy and commodity prices are buoyed as productivity-induced supply gains cannot keep pace with emerging-market demand. As might be expected in such an environment, employment growth rebounds and most countries see unemployment rates fall and participation rise. India, China, and commodity-driven economies account for 80 per cent of employment growth. Elsewhere, policy changes in advanced economies encourage aging workers to stay in the workforce longer, while making it easier for women and part-time workers to stay employed.

SCENARIO 2

POCKETS OF GROWTH: DIVERGENCE WITH RAPID GROWTH

In this second scenario, the growth picture becomes more uneven, as countries tackle structural challenges in fits and starts. Global growth reaches 3.2 per cent a year over the course of the decade, a relatively high historical level, and by 2025 the global economy reaches $88 trillion in 2015 dollars.

The U.S., China, and India achieve satisfactory and even sporadically robust growth, while the eurozone and Japan struggle. The unevenness of the expansion makes agreements harder to reach on international protections for investors, intellectual property, and agricultural subsidies. As a result, trade growth starts to slow and remains effectively flat relative to GDP at 25 per cent.

Some countries find it difficult to exit from unconventional monetary policies, which continue to distort credit channels and capital flows. The search of investors for higher or more stable yields quickens, adding to volatility. Oil prices gradually revive on higher demand, and producers of other commodities encounter more frequent supply constraints.

SCENARIO 3

GLOBAL DECELERATION: CONVERGENCE WITH SLOWER GROWTH

This lower-growth scenario is defined by global convergence to a slower path. Global growth manages to reach 2.9 per cent over the course of the decade, slightly below average for the past three decades. The expansion is especially reliant on positive outcomes in emerging markets. By the end of the decade, the global economy reaches $86 trillion in 2015 dollars.

Structural challenges remain largely unaddressed, but are offset in the near term by partly successful efforts to revive demand. China avoids the worst effects of a ‘hard landing’, but confidence in the fiscal system is shaken, further weighing on growth. China still accounts for nearly 23 per cent of global GDP by 2025, however. In the advanced economies, fiscal and monetary buffers to address structural reforms are exhausted.

Near-term demand revives globally, creating an opportunity for Europe and the U.S. to make progress on financial services, privacy, and M&A activity, which becomes a benchmark for global emulation. Trade is a more important driver of growth in this scenario than in the previous one. The lower growth curve is a constraint, but trade still accounts for 27 per cent of the global economy. Demand for energy (including oil) revives, but the availability of additional supply keeps prices from recovering more quickly.

SCENARIO 4

ROLLING REGIONAL CRISES: DIVERGENCE AND LOW GROWTH

This final scenario is the negative image of the global-synchronicity scenario. Growth stalls and the world economy is $11.4 trillion smaller than it would be in that scenario. ‘Rolling regional crises’ describes a world where structural reforms broadly stall, and aggregate demand, especially in advanced economies, does not return in a sustainable way. Deleveraging remains a drag on household balance sheets, and corporate-debt levels continue to rise.

Increasingly, countries rely on conventional and unconventional forms of fiscal and monetary stimulus. Real interest rates remain in negative territory, but the growth outlook fails to encourage renewed investment growth. Incremental fixed investment in the G-20 countries totals little more than half the level in the global-synchronicity scenario.

With not enough economic incentive, companies fail to invest in R&D and technological innovation remains confined to a few regions. The diffusion of technology also slows down as economies increasingly turn inward. Implicit and explicit restrictions on international M&A activity proliferate, as do regulations inhibiting the expansion of trade and technology. As a result, the share of exports in GDP for G-20 nations rises more slowly, from 31 per cent today to 34 per cent by 2025. Similarly, employment growth slows and the G-20 nations add 60 million fewer jobs than they would in the global-synchronicity scenario. In a repeat of the 1980s, global oil supplies remain abundant and energy prices stay flat in real terms.

In this scenario, the world economy remains much more vulnerable to economic shocks, particularly from financial flows. Low interest rates, combined with expanded financial liquidity, create the conditions for volatile flows seeking yields in response to the slightest hint of a change in the growth outlook.

In closing

Our scenarios suggest that the major economies face significant structural challenges. To revive growth, these countries must tackle the challenges while navigating constant reverberations from an interconnected world economy. For strategists, the course of trade and information flows is of crucial importance, as the direction and forces behind the flows determine how industries will be affected. For instance, rising south-to-south trade in goods creates a very different set of opportunities than does increased services-driven trade or increased investment based on production location.

Volatility and shocks are an ever-present feature of the world economy. Unfortunately, in many parts of the world, the policy tools and financial reserves needed to absorb such shocks have been expended in dealing with previous events. Understanding susceptibility and resilience to shocks — from a national and global perspective — will allow strategists to make better decisions about market entry, new investment or market exit.

We hope that the scenarios laid out herein will be helpful to leaders in their strategic planning. They have been designed as baselines against which different corporate strategies can be tested, to reveal how industry-specific dynamics may evolve in response to macroeconomic shifts. We believe that most companies will find that regular pressure testing of their strategies in response to both macroeconomic and industry shifts helps to sustain growth in the face of challenging conditions.

Click here for a PDF version of this article.

Luis Enriquez is a Director in McKinsey & Company’s Brussels office. Sven Smit is a Director in the Amsterdam office. Both are leaders in McKinsey’s Global Economics Intelligence group. Jonathan Ablett is a Knowledge Expert with the McKinsey Global Institute. This article was originally published by McKinsey & Company, at McKinsey.com. Copyright 2015. Reprinted by permission.

This article originally appeared in 'The Global Mindset Issue' (Spring 2016).