MOST PEOPLE GROWING UP in advanced economies since World War II have assumed that they and their children will be better off than their parents and grandparents — and for most, that assumption has been correct. Over the past 70 years — except for a brief hiatus in the 1970s — buoyant economic growth has meant that all households, especially those of the Baby Boomer generation, experienced rising incomes, both before and after paying taxes and receiving government transfers such as unemployment or social security benefits.

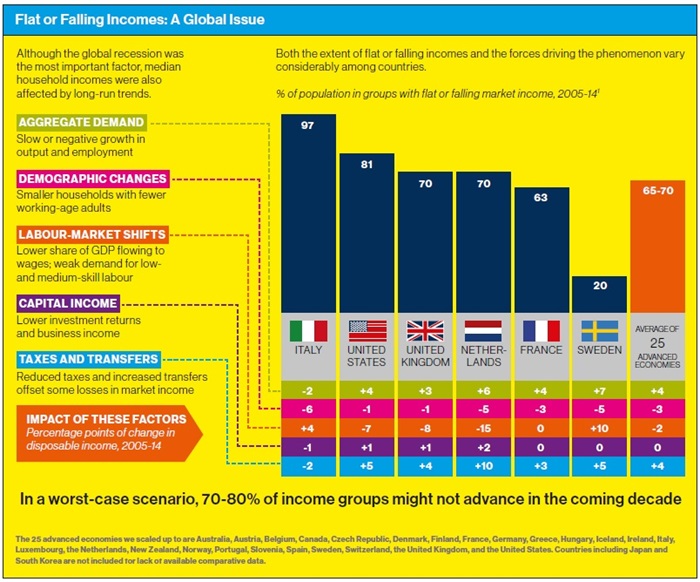

This positive income trend has come to an abrupt halt in recent years: Our research shows that in 2014, between 65 and 70 per cent of households in 25 advanced economies were in income segments whose real market incomes — from wages and capital — were flat or below where they had been in 2005. This does not mean that individual households’ wages necessarily went down, but that households earned the same as or less than similar households had earned in 2005, on average. In the 12 preceding years, between 1993 and 2005, this ‘flat or falling’ phenomenon was rare, with less than two per cent of households not advancing. In absolute numbers, while fewer than ten million people were affected in the 1993–2005 period, that figure exploded to between 540 and 580 million people in 2005–14. Taxes and transfers to helped soften the blow, but disposable incomes were nonetheless flat or down in 20 to 25 per cent of income segments, on average.

The severe recession that followed the 2008 financial crisis and the slow-growth recovery since are a fundamental cause of this phenomenon, but we found that deep-rooted demographic and labour-market factors have also played a role — and will likely continue to do so, even if economic growth accelerates. These factors include shrinking households, a smaller share of GDP going to wages, and increased automation in the workplace. Even in the 2005 to 2014 period, market incomes in most of the countries we studied would have risen slightly had it not been for such changes.

In this article, we will summarize the factors underlying the ‘flat or falling phenomenon’ and outline some options for dealing with what is potentially a corrosive social and economic development.

The Flat-or-Falling Phenomenon

There are several ways to think about income inequality and its implications. The most common approach in recent years has been to look at the rising gap between the wealthiest segments of the population and those in the middle or lower end of the scale. This, for example, has been the focus of French economist Thomas Piketty, whose best-selling book about the concentration of wealth going to top earners sparked broad public discussion. Another frequently used approach is to focus on the poor — those with insufficient income to provide for their basic needs, often calculated as a percentage of the median income.

Our research looks at a third aspect, which has not been as widely studied: The rapid growth in the proportion of income segments in advanced economies whose earnings both before and after taxes and transfers have been flat or falling. This goes beyond the degree of inequality measured in the standard Gini index by providing a detailed view of the trajectory of all income segments, which can be lost in a consolidated index. We focus on income rather than on wealth or consumption, and we also look at the evolution of incomes over time, rather than at a fixed point.

We used three approaches to analyze this flat or falling phenomenon. The first looked at changes by income segments, or households divided into deciles (tenths), quintiles (fifths), and even percentiles (one-hundredths), depending on where they rank in the national income distribution. We examined income segments in six advanced economies — France, Italy, the Netherlands, Sweden, the United Kingdom and the United States — to determine how they have fared over the past two decades. We then scaled up the findings to include 19 other advanced economies — including Canada — with similar growth rates and income distribution patterns, for a total of 25 countries with a combined population of about 800 million that account for just over 50 per cent of global GDP.

Our second approach was an analysis of a detailed data set for 350,000 people in the three countries, with microdata available — France, Italy and the U.S. For these countries, we examined income by age bracket and educational attainment. Finally, we sought to understand perceptions through conducting detailed surveys of more than 6,000 people in France, the UK and the U.S. that tested how people felt about the evolution of their income.

Our first key finding: Since 2005, household incomes across advanced economies have stagnated or fallen for most income segments. This is based on an analysis of income segment data from national agencies in the six countries we looked at in detail, a total of 487,000 households. On average, 65 to 70 per cent of the population were in income deciles (10-per cent slices of the population) whose real market incomes in 2014 fell compared with 2005. In our six focus countries alone, more than 400 million people were in income segments with flat or falling market incomes. When scaled up to the 25 countries in our sample, this translates into 540 to 580 million people.

Income from wages fell for all population segments between 2002 and 2012, regardless of age or level of education.

By comparison, in the 12 previous years, between 1993 and 2005, less than two per cent of the population — fewer than 10 million people — were in income segments whose average market incomes were flat or down. The impact was smaller when measured in disposable income; but even after accounting for higher net transfers to households because of the recession, disposable incomes, on average, were flat or down in 20 to 25 per cent of income segments.

The distribution of flat or falling incomes varied across the six economies we studied in depth. At one extreme was Italy, which experienced a severe economic contraction in the recession after the 2008 financial crisis and has had a very weak recovery since. There, real market incomes were flat or falling for virtually the entire population. At the other extreme was Sweden, where only 20 per cent of the population had flat or falling incomes. In each of the four other focus countries — France, the Netherlands, the UK and the U.S. — the proportion of segments whose market incomes did not advance was in the 60-to-80 per cent range.

The variation was even greater at the level of disposable income: The share of income segments whose disposable income did not advance between 2005 and 2014 ranged from 100 per cent in Italy to 10 per cent in France and less than two per cent in Sweden and the U.S. These variations reflect widely varying national economic, fiscal and monetary policy responses to the recession.

The trend of flat-or-falling incomes was confirmed by our second analysis of age- and education-based population segments. Our data on 350,000 individuals from France, Italy and the U.S. tracked incomes of demographic segments based on three age brackets (younger than 30, 30–45, and older than 45) and three levels of educational attainment — low, medium and high, based on whether a person received less than a high school diploma, a high school diploma, or a bachelor’s degree or above.

This second set of data confirmed our results from the first analysis by income segments: We found that income from wages fell for all population segments between 2002 and 2012, regardless of age or level of education. In all three countries, less-educated workers, and especially younger ones, have been most affected. Moreover, the recession and weak recovery have led to persistently high levels of youth unemployment, preventing young people across advanced economies from launching careers. These are the people who are literally at risk of growing up poorer than their parents.

Women were also over-represented in lower-income deciles. Single mothers were more likely to be in segments that were not advancing, although there was a variance among countries. In the U.S., 20 times as many single mothers were in the lowest-income decile as in the highest. In Italy, there were eight times as many single mothers in the lowest income households as in the highest-income households. For France this number was 11 times.

Our microdata for the U.S. show that single-mother households not only earn less than the average household, but their real household income also declined nearly one percentage point faster than all other households in the decade from 2003 to 2013.

The citizen surveys we conducted in 2015 in France, the UK and the U.S. show that perceptions are in line with the findings of our analysis of income and population segments. We sought to gauge whether people perceived a decline in their income by asking them to respond to statements about their financial position today, whether it had improved, and how it compared with that of friends and neighbours. We also asked what they expected their financial position to be in five years’ time, and whether they thought they were worse or better off than their parents at the same age.

Declining earning power for large swaths of the population could limit demand growth and increase the need for social spending.

While the answers varied by country, overall, there was an even split, with 30 to 40 per cent saying their incomes were not advancing, and the same proportion saying their incomes had advanced. The remaining 20 to 30 per cent were neutral and did not feel strongly either way. The 30 to 40 per cent who felt they were not advancing held more pessimistic views about their futures and the futures of their children than those who felt they were advancing. Nearly half of those not advancing expected not to advance in the future, compared with just one quarter of those who felt they were advancing. Those who felt they were not advancing fell into one of two camps: The two-thirds who believed that things would improve for their children and the next generation, and the remaining one-third, who saw slow income growth as a persistent problem that would continue to affect their children.

Over time, declining earning power for large swaths of the population could limit demand growth in economies and increase the need for social spending and transfer payments, even as tax receipts from workers with stagnating incomes limit capacity to fund such programs. The impact could be more than purely economic, however, if the disconnect between GDP growth and income growth persists.

Our survey provided an indication of the potentially-corrosive social and economic consequences of flat-or-falling incomes. Along with questions about income trends, we asked about people’s views on trade and immigration. The citizens who held the most negative views on both were the same group who felt their incomes were not advancing and did not expect the situation to improve for the next generation. More than half of this group agreed with the statement, ‘The influx of foreign goods and services is leading to domestic job losses,’ compared with 29 per cent of those who were advancing or neutral. They were also twice as likely to agree with the statement, ‘Legal immigrants are ruining the culture and cohesiveness in our society’.

Those who were not advancing and not hopeful about the future were also more likely than those who were advancing to support nationalist political parties such as France’s National Front or, in the UK, to support the move to leave the European Union.

What Can Be Done to Advance Incomes?

For government policymakers and business leaders alike, introducing changes that rekindle income advancement is notstraightforward and may require some difficult trade-offs. Policies to raise productivity may not help reduce income inequality, for example, while efforts to achieve a more equal income distribution may at times inhibit moves to increase productivity growth. Following are four policy options aimed at stimulating discussion.

1. CREATE MEASUREMENT TOOLS TO GAUGE THE EXTENT AND EVOLUTION OF FLAT OR FALLING INCOMES

International organizations including the OECD and the International Labour Organization (ILO) are starting to look at more effective ways to measure income inequality, alongside other standard economic indicators such as unemployment or GDP growth. Income advancement could become a policy goal in its own right, a fundamental indicator of the health of the economy and society, comparable to poverty reduction or sustaining overall employment.

To address the issue of flat-or-falling incomes effectively, policymakers will need to adopt specific metrics to track the phenomenon across the entire income spectrum. For now, such data are not systematically gathered in most countries, and where statistics are available, they tend to be based on survey data. Measuring flat-or-falling incomes is an important starting point to provide a fact base, and the metrics could be improved, including through use of more reliable sources such as tax data.

Tracking this data could be part of the formal mandate of international organizations including the OECD or the World Bank so that it can be aggregated and compared across countries. As different policies are deployed around the world, they could be structured in a way that would enable their outcomes to be measured. Tracking and evaluating flat or falling incomes would allow for the development of a set of best practices that could be deployed across countries.

2. REVIVE GROWTH AND ENABLE A THRIVING BUSINESS ENVIRONMENT THAT CREATES JOBS

As we have seen, the economic downturn was a fundamental cause of the lack of income advancement for a large majority of income segments since 2005. The corollary is that revival of stronger economic growth will be a key to raising incomes, even in the face of demographic shifts and labour-market changes that work against them. Conversely, if the current low-growth world becomes ‘the new normal’, flat-or-falling incomes could become entrenched.

The paramount importance of boosting growth through improved productivity is a theme we have researched extensively. About three-quarters of the potential for productivity improvements comes from the adoption of existing best practices and ‘catch-up’ productivity improvements, while the remaining one-quarter comes from technological, operational and business innovations that push the frontier of the world’s GDP potential. Governments have many opportunities to help boost productivity, including through measures that would reduce waste and improve resource and energy efficiency, increase competition and deregulation, or target infrastructure and other investment that creates new jobs in the short run and shores up economic growth over the longer term.

3. DEVELOP MEASURES AIMED AT HOUSEHOLDS MOST AT RISK

Beyond such general remedies, the phenomenon of flat-or-falling incomes could be addressed through measures specifically aimed at low and middle-income households or the population segments we identify as being most at risk, including young people with low educational attainment, women and older workers.

Upgrading skills and easing the transition from education to employment is one approach. At the secondary school level, public school systems can collaborate with local businesses to craft vocational training and apprenticeship programs, particularly in fast-growing service industries such as healthcare. Governments and businesses could work with universities and other post-secondary institutions to expand access to quality education and ensure that the learning provided is relevant to the workplace of tomorrow. And incentives could be offered for students to pursue fields of study such as science, technology, engineering and math, which lead to more lucrative jobs.

To raise labour participation among women and older workers, policymakers could provide greater access to child care, or help women enter or re-enter the labour force by removing tax rules that penalize two-income households. Technology could also provide some solutions. Digital platforms such as LinkedIn or Monster, which link employers with workers, provide a new way of overcoming a skills mismatch, while companies such as TaskRabbit provide opportunities to become engaged in independent work.

Income advancement could become a policy goal in its own right, a fundamental indicator of the health of a society.

We estimate that such online platforms could increase global GDP by two per cent between now and 2025. Enforcing antidiscrimination laws would also help raise incomes for women and minority segments, while pension reforms can reduce the proportion of workers who leave the labour force early.

4. USE TAX AND WELFARE POLICIES TO SECURE DISPOSABLE INCOME GROWTH

Many advanced economies used transfer and tax policies to battle the effects of the recession and its aftermath. Fiscal stresses and mounting government debt can make raising taxes and transfers economically challenging today and in the future. But rather than implementing broad-based redistributive programs, policymakers can use tools targeted at income deciles with flat-or-falling incomes that are not as costly.

For example, even where national income taxes are low, sales and value-added taxes, payroll taxes and property taxes can fall heavily on low and middle-income households. These taxes could be adjusted to raise disposable incomes for these households. Policymakers can also consider the impact of their spending

decisions on disposable incomes of segments whose incomes are not advancing. A public transit system, for example, is likely to provide more value for a lower income household than a new highway.

Where there is political consensus, direct payments such as a guaranteed basic income scheme could be used to maintain disposable incomes. Also, where appropriate, labour rules could help lift incomes for segments that have not been advancing. This might include adjusting minimum wages or extending employment benefits to part-time and temporary workers, which some countries have already done.

The Role for Business Leaders

Flat-or-falling incomes — and the underlying causes for them — raise questions about how businesses can thrive over the long term in advanced economies. The declining purchasing power of the broad middle classes in consumption-driven economies is the most obvious problem. Another arises from one of the most

important causes of income stagnation: Escalating demand (and cost) for high-skill labour and falling demand for other types of workers. This is creating a potentially-serious shortage of highskill talent across advanced economies and a glut of less-skilled workers.

Business leaders have a legitimate role to play in shaping the discussion on flat-or-falling incomes and helping to create solutions. CEOs can be advocates for the investment and growth necessary to create employment. They may recognize that paying better wages and introducing profit-sharing and non-cash benefits can raise employee disposable incomes and at the same time, raise productivity and loyalty. Companies can also benefit by taking steps to keep women and older workers in the workforce.

Finally, companies can invest in a better labour pool — and increase the earning potential of workers — by collaborating with the public sector on job-relevant education. More broadly, companies can act as catalysts in their communities to enact policy changes.

| |

|

|

| |

Why Incomes Stopped Rising

|

|

| |

- Aggregate demand factors. When aggregate demand (or GDP) grows, employment and labour-force participation also increase, enabling incomes to rise. Conversely, lower labourforce participation rates, rising unemployment, and waning productivity (output per worker) can all lead to stagnating or falling incomes. Unemployment in particular can have a dampening effect on household income.

- Demographic factors. These capture changes in the number of working-age people in each household. This number has fallen in several of our focus countries because of the shrinking size of households, the result of changing family structures, lower fertility rates and aging, which decreases the number of people available to work.

- Labour-market factors. These include the evolving pattern in labour demand and supply. This is manifested in the wage share of GDP and the median household’s share of wages. Among the forces that can explain movements in these two factors are income gains for high-skill workers and negligible income gains or declines for low- and medium-skill workers, and the share of part-time and temporary work, which is often less well paid than full-time work. Labourmarket factors can vary depending on the role and influence of unions, different national labour regulations and practices, trade and immigration, and the degree to which jobs are affected by automation.

- Capital income factors. These include capital gains from asset sales, interest and dividends from investments, rental income, income from business, or income received from private pension plans.

- Tax and transfer factors. Transfers include a range of cash payments to beneficiaries such as social security payments, disability or workers’ compensation, and unemployment benefits. The first three of these categories—aggregate demand, demographic, and labour-market factors—contribute to changes in labour income. Changes in market income are driven by changes in this labour income, together with changes in capital income. Disposable income is the amount households receive after taxes, and transfers are applied to market income.

|

|

Richard Dobbs is a Director of the McKinsey Global Institute (MGI) and a Senior Partner, based in McKinsey & Company’s London office.

Anu Madgavkar is a Partner with MGI, based in McKinsey’s Mumbai Office.

James Manyika is a Director of the MGI and Senior Partner in McKinsey’s San Francisco office.

Jonathan Woetzel is a Director of the MGI and a Senior Partner in McKinsey’s Shanghai office.

Jacques Bughin is a Director of MGI and a Senior Partner in McKinsey’s Brussels office.

Eric Labaye is Chairman of the MGI and a Senior Partner based in McKinsey’s Paris office.

Liesbeth Huisman is a former Engagement Manager at McKinsey’s Amsterdam office.

Pranav Kashyap is an Engagement Manager at McKinsey’s Silicon Valley office. The complete report on which this summary is based can be downloaded online.

This article originally appeared in The Inequality Issue (Fall 2017) of Rotman Management. The magazine offers the latest thinking on leadership and innovation and is published three times a year.

Share this article: